“It will purge the system,” said Secretary of the Treasury Andrew Mellon to President Herbert Hoover after the stock market crash of 1929. “…High costs of living and high living will come down. People will work harder and lead a more moral life. Values will be adjusted and enterprising people will pick up from those less motivated.”

Some eighty years later, Bill Gary wrote the following in The Dow Theory Letters:

“It is becoming clearer each week the life we have known has been changed forever. No longer can many afford to dine at fancy restaurants, buy designer clothes, make payments on a new Porsche or purchase a McMansion… We took out home equity loans to pay for vacations…We measured wealth by the limit on our credit cards. Now the dream of perpetual prosperity has ended.”

In other words, the mess we are in now is not unique. It has occurred twice in the Nineteenth Century and at least once in the Twentieth. It will happen again, too.

Riding the Waves

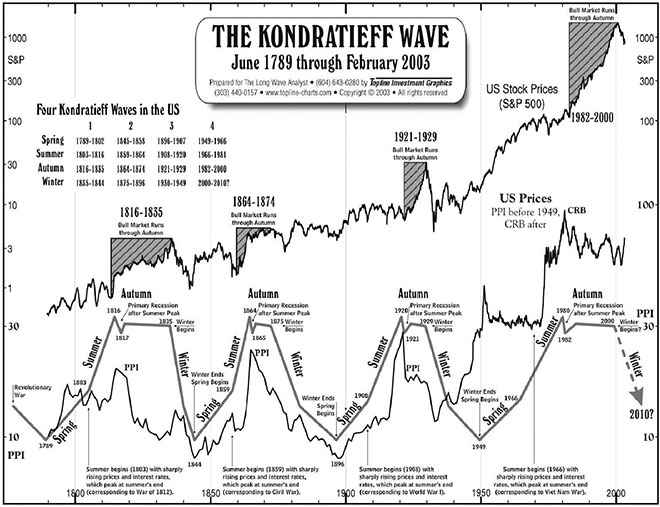

A little-known Russian economist named Nicoli Kondratieff, who worked at the Ministry of Agriculture in Moscow, made an important discovery in the 1920s. By analyzing a series of interest rates together with raw and historic finished material prices in France, Britain, and the U.S., Kondratieff found that there had been cycles of booms and busts every forty to seventy years (see diagram 1). Kondratieff’s communist bosses were delighted when he forecast a crash of capitalism in 1929, but less pleased with its subsequent recovery. The Russian bureaucrat finished his days alone in Siberia.

The first wave, K1, started in George Washington’s second term and, as often happens during unification, this led to a boom, which was accelerated by the Louisiana Purchase and the expenditures associated with the 1812 War. The economy peaked in 1816, before a short recession, which was followed by a plateau phase of nineteen years before the downturn. The downturn lasted through the “hungry forties.”

The second wave, K2, was largely driven by the accession of Texas, New Mexico, Arizona, and California to the U.S. after the Mexican War (1846-1848), which led to the gold rush that fueled the boom. The new railroads that joined the Midwest to the east coast also contributed to the prosperity. The end of this wave came at the conclusion of the Civil War in April 1865. A post-war recession, exacerbated by failures in the nascent railroad sector, followed for more than two decades.

The third wave, K3, was probably driven by the advent of Henry Ford’s mass production of the Model-T, exuberance over winning the Spanish American War (1898), and the celebrated presidency of Theodore Roosevelt. The boom was accelerated by the arms production of World War I. However, the “Roaring Twenties” were followed by the stock market crash. By 1932, the GDP had declined by thirty percent in real terms. This recession lasted until 1949, just before the Korean War.

Diagram 1

The latest cycle is the most exuberant of all, marked by the rapid rise in U.S. stock prices and, as will be shown in the next diagram, a massive rise in debt, and the accompanying credit required to generate extra dollars of GDP. However, by 2008 the ability to increase additional output was fading. In his book Debt and Delusion, Peter Warburton shows how the effectiveness of credit stimuli reduced with time; one dollar of debt only added one cent of output.

The upwave began with the Korean War in 1950, which was followed by a booming domestic economy. The hiatus in the early 1970s was the result of a rapid rise in oil prices, followed by a recession later in the decade. However the real end of the upwave was marked by the panic of 1980, followed by a deep recession before reaching a plateau phase that lasted nineteen years (the longest since K1).

The beginning of the most recent downwave was caused by the bursting of the dot-com bubble and the frantic efforts by the Federal Reserve Bank to avoid a recession by creating excess money that led, as in the 1920s, to new bubbles in housing and other markets. As we reach the end of the first decade of the new century, we are now in the early stages of “debt deflation,” which we will explore below.

Kondratieff, for his part, never gave reasons for his waves. This was left to Joseph Schumpeter, who became known for his work on business cycles. The great economist believed in “innovation cycles” whereby swarms of inventions at a particular time fed off each other to create an upwave, only to crash when the innovations became obsolete.

K-waves are essential to understanding economic trends. However, the length of the cycle is such that wisdom often skips a generation, jumping from grandparent to grandchild, so we never learn from our mistakes.

Debt

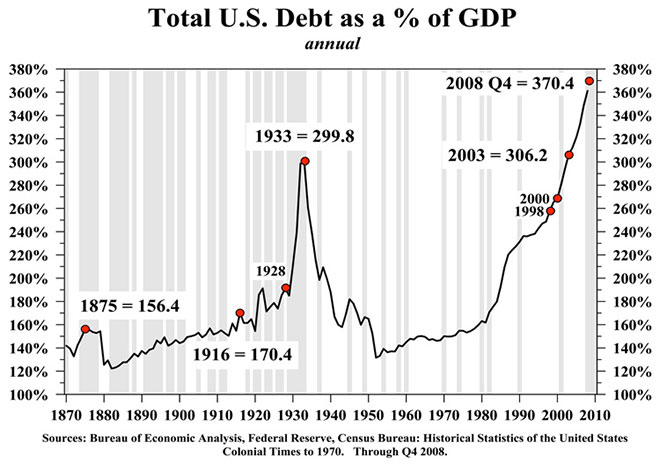

Milton Friedman, in his Monetary History of the United States, rejected the Keynesian view that the Great Depression could be cured by government spending, and suggested instead that the 1929 crash was caused by a monetary deficiency. By contrast, Irving Fisher believed the crash was caused by debt. He called it “debt deflation,” depicted in a pattern over the last one hundred and forty odd years, as seen in the next diagram.

This diagram depicts the debt history of the USA through the downwave of K2, the complete cycle of K3, and the upwave and plateau of K4 (from our first diagram).

Diagram 2

Although debt started to rise in 1880, the true boom started in the 1890s and continued steadily to the recession in 1920. It continued into 1929, when the ratio peaked at 195 percent. At that time, the U.S. government was minimally borrowed; the majority of debt was private. When the economy declined by thirty percent, the ratio rocketed to reach nearly 300 percent in 1933. The rate subsequently fell to 160 percent by the time of Pearl Harbor, when government debt began to rise to pay for the enormous war effort. Output, however, rose almost as fast before collapsing once again to below 140 percent in 1949. In all, the debt destroyed between 1929 and 1950 was $100 billion, just under the GDP in 1929.

The rise in the ratio in the Reagan years was about the same level as K3, but the rearmament in the 1980s to defeat communism accelerated the rise before slackening around 1990.

The acceleration resumed to 360 percent 2008. Extrapolating from the data of the early 1930s, the ratio could rise to well over 400 percent before collapsing. If the ratio is to return to 180 percent, and with the GDP declining by ten percent from around $14 trilllion, the amount of credit to be extinguished in K4 could be well in excess of $20 trillion by 2015.

Glimpsing The Future?

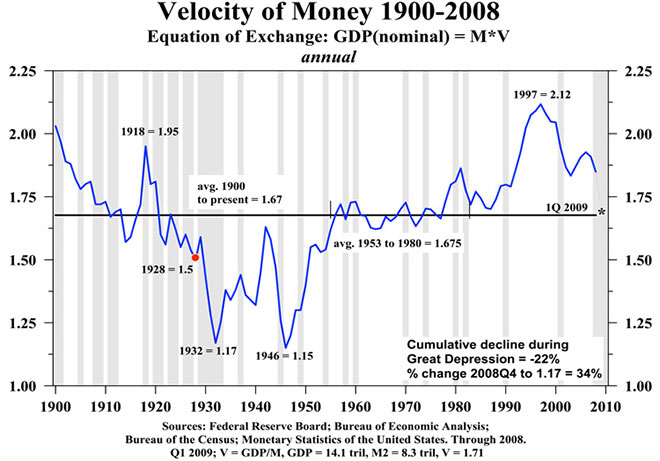

The quantity of money theory holds that money supply, multiplied by the rate of circulation (the velocity), equals the nominal GDP. As the third diagram shows, regeneration of the GDP will be very difficult to achieve in a recession until the velocity becomes positive once more.

Diagram 3

During K3, the ratio peaked in 1918. Then, as the caption shows, it declined 22 percent during the Great Depression, followed by another post-war dip before the recovery at the early part of K4. It hovered around 1.675 for much of the upwave, only to rocket to 3.12 in 1997 towards the end of K4 plateau phase. Technicians would call this an inverted ‘head and shoulders’ formation. The data suggests that a collapse to 1.17 would imply a fall of 34 percent, which could take us well into a second decade.

This would not come as a surprise. We are now in a credit cycle where debt is so high that lowering interest rates will not bring recovery. Moreover, increased government spending may deprive the private sector of low cost funds. Thus, despite the euphoria over the G-20 on April 2, 2009, there are reasons to remain skeptical that the world is ready to move out of recession.

Climatic Change

It may also be important to consider the impact of the climatic conditions on the recession. In 1789, the year of the French Revolution, a combination of drought, crop failures, decaying public finances, and poverty inflamed what would otherwise have been an orderly transfer of power.

Climatic shifts may also be responsible for stagflation on a greater scale. Dr. Lacy Hunt of Hoisington Investment Management has shown that supply-side climatic problems could well create rises in the prices of food, raw material, and energy that are difficult to quell without deepening the downturn. Under such conditions, stagflation is possible. In the mid-1970s, when Americans experienced a condition where the rising prices of a range of commodities were imposed against a stalling economy. This presents decision makers with a dilemma: do they raise interest rates to slow inflation and risk an even deeper recession, or do they allow the cost of inflation to rocket?

Looking ahead, to ensure continued food supplies, new technologies and programs will be needed to regenerate arable land taken out of production, to radically improve the techniques of irrigation, and to introduce cultivars adapted to strenuous climatic conditions.

The Digital Age

While every K-wave had its own pattern, each was sparked by a new activity, idea, discovery, or personality, and each ended with collapsing credit. Each cycle appears to clear away redundant activities to make way for the new. As such, the current downwave may have an additional role: to jettison the debris of the industrial age. For three hundred years, the power of governments, money, and large-scale operations has grown. They could be about to collapse under the pressure of the Digital Age where the individual is empowered and the state plays a lesser role. (On a side note, it would be ironic if the London G-20 summit, hailed as the apotheosis of big government power, led to its downfall).

The entry to the Digital Age will produce a new set of problems and opportunities. This will be the age of the individual; brains, initiative, and character will be more important than political or financial clout. The new age may necessitate radically smaller governments that absorb less than thirty percent of GDP. It may well need an environment for entrepreneurs to thrive with minimum taxation, regulation, and interest rate burden.

More importantly, the Digital Age will require a new era of innovation. The fracturing of global capital and banking markets will almost certainly need new methods of raising capital. New jobs (and new education programs) will be required to compensate for those rendered redundant. New technologies will focus on transportation, agriculture, communications, medicine, manufacturing, and probably also defense. (Most K-waves in the upwave or downwave have ended with conflicts).

The transition out of the current recession will thus require the talents of extraordinary people against many entrenched positions. History shows such individuals emerge from societies where the state exists for the individual. And it is always the private sector in such societies, not the public sector, that brings economies out of recession.

William Houston, the author of Riding the Business Cycle and six other books, is a London-based senior economist specializing in corporate turnarounds. He wrote this piece on behalf of the Noah Group, an economic forum headed by JPC Chairman Richard Fox.